Competition Raises Health Insurance Rates In Northern California –

With the addition of a new competitor in Northern California’s San Mateo County, some Covered California plan members have seen their monthly health insurance rates increase by over 100 percent. Whereas we normally assume that competition in the market place drives prices down, in this case, because of the Affordable Care Act formula for determining the subsidy, a new health plan in San Mateo County has caused the rates to spike up.

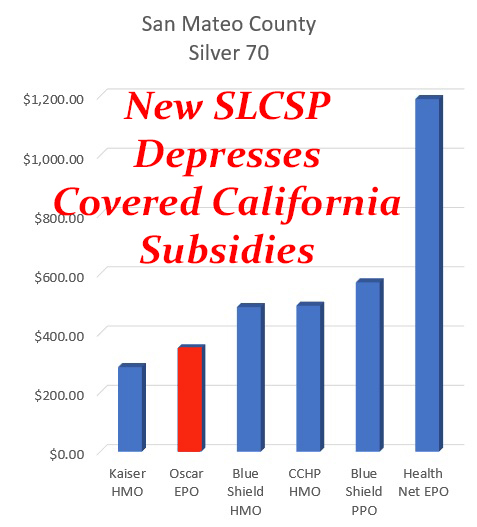

At the center of the matter is the addition of Oscar health plans expansion into San Mateo County. Oscar became the new Second Lowest Cost Silver Plan (SLCSP.) Because both the federal and California subsidies are based on making the SLCSP affordable, many consumers are receiving a smaller subsidy for 2021. The smaller subsidy combined with regular rate increases and an increase for their age meant they are paying substantially more for their health insurance in 2021.

New Health Plan Competitor Reduces Subsidies, Increases Rates

I had received several calls from clients in San Mateo County asking me to explain why their rates had double or tripled in 2021 compared to 2020. Part of the annual increase is explained by the carrier’s overall rate increase across all plans. Except for Health Net in San Mateo County, most of the carriers had modest rate increases. The second part of the rate equation is that the rates are based on age. For adults, there will be an average increase of between 4 to 7 percent for aging one year.

The final part of the equation is how the Covered California subsidies are calculated to make the SLCSP affordable under the ACA formula for reducing health insurance premiums. If the SLCSP rate increases more than your selected health plan, you get a bigger bump in the subsidy. If the SLCSP decreases relative to the prior year, the subsidy will be smaller.

Lower Second Lowest Cost Silver Plan

However, all of those factors did not fully explain the enormous jump in monthly health insurance premiums my clients were facing in San Mateo County. Upon closer inspection, it was evident that the expansion of the Oscar health plans into San Mateo County was the disruptor in the equation. The Oscar rates, in most cases, were higher than the least expensive Silver plan (Kaiser) and under what would have been the SLCSP plan (Blue Shield HMO.)

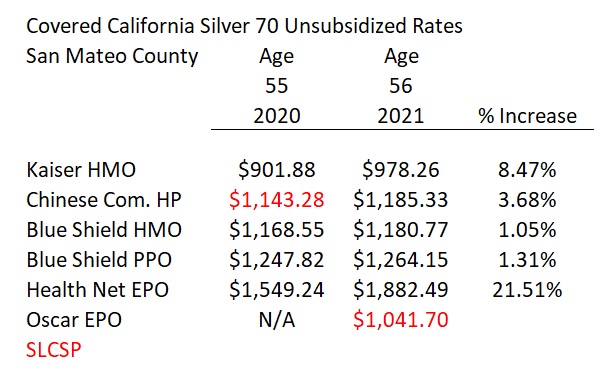

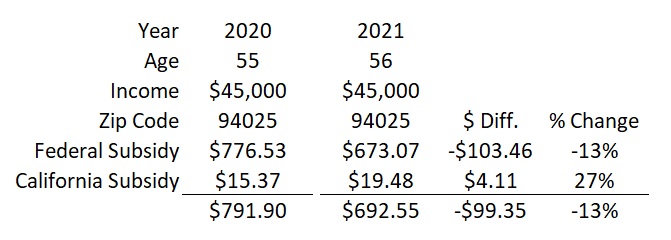

To verify the subsidy decrease because of the new Oscar health plans, I used Covered California’s Shop and Compare Tool to calculate the subsidy for an individual in San Mateo County with an annual income of $45,000. In 2020 the individual was 55, and in 2021 I used the age of 56. The overall decrease in subsidy was approximately 13 percent or $100 per month.

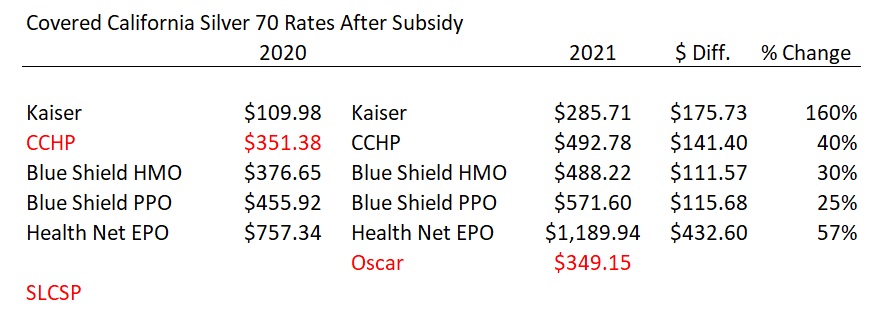

The Shop and Compare Tool calculated the subsidized rates for each Silver 70 health plan for 2021. When compared to 2020, the monthly health insurance premium for the 55-year-old individual increased between 25 and 160 percent. Kaiser, the least expensive Silver plan, had the largest dollar increase of $175 per month. Without the Oscar expansion, the Blue Shield HMO Silver 70 would have been the SLCSP, but the much less expensive Oscar Silver plan came in second, $139 lower after the subsidy. The full rate for Oscar Silver plan is 13 percent less expensive than what should have been the SLCSP, the Blue Shield HMO. Does 13 percent ring any bells? That is the amount of the decrease in the annual subsidy for the 55-year-old in 2021.

The Bronze plans had similar increases because of the decrease in the subsidy. The 55-year-old would have paid $1 in 2020 for the Kaiser Bronze 60 plan. In 2021, the Kaiser Bronze 60 is $98. Both the Chinese Community Health Plan and Blue Shield PPO Bronze plans have increases of over $100, and over $300 for the Health Net EPO.

Blame It On The ACA, Not Competition

In reality, competition plays a very minor role in reducing health insurance rates. The big drivers of the rates are expected health care services within a given population and the contracted rates for those services. The presence of the Oscar health plans in San Mateo County did not depress the other carrier’s rates. There was already a big differential between the least expensive Silver plan (Kaiser) and the SLCSP Blue Shield HMO for 2021 of $202.51.

Had Blue Shield HMO been the SLCSP for 2021, and because the rate is so similar to the Chinese Community Health Plan – only $5 difference – most San Mateo County consumers would not have seen much of a difference in their rates. But because Oscar came in 13 percent below Blue Shield HMO and Chinese Community, the lower SLCSP depressed the subsidy amounts.

The lower subsidy is not the fault of the carriers or market place competition. The increased monthly premiums are solely the function of the Affordable Care Act formula for determining the subsidy. The subsidy formula does not take into account new health plan rates that have the potential for radically depressing the subsidy.

This content was originally published here.

Responses