What I’ve learned about health insurance – FineWoodworking

This post comes from hard-won experience – the kind from which I hope to help save you. I know a lot of self-employed people who don’t have health insurance because they say they don’t need it, can’t afford it, or it’s going to cost too much and “not pay for anything anyway.”

I get it. Health insurance premiums are expensive, especially if your household income is just high enough to disqualify you for any subsidies the Affordable Care Act (ACA) offers in an effort to make medical coverage affordable. Many woodworkers have a spouse who gets family health insurance through a group policy as a benefit related to employment. If you’re one of them, great. But if you, like my husband and me, have to go it alone, you owe it to your family and yourself to research the policies that are available and get coverage.

I have been buying health insurance since 1995, when one of my customers broke his ankle in a fall and ended up having to pay $2,000 of his $10,000 hospital bill. As a tenured professor at our state university, this customer had excellent coverage, and his premiums were enviably low. Yet he still had to pay $2,000, a sum that could easily have put my fledgling business out of commission. As soon as I heard about his plight, I contacted my insurance agent and arranged for coverage.

I was healthy and in my mid-30s at that time, so the premiums were low. (Not all states base, or based, premiums on age. Some base them on zip code and standardize rates for all.) Still, when you’re self-employed, income can be sporadic — feast or famine. At numerous times over the succeeding 25 years, paying those premiums has been a struggle. But I considered them no less important than paying my mortgage. As a professional in the building trades, I’m well aware of how easily I could be injured and rack up medical bills that might bankrupt me.

When the ACA went into force, my husband, Mark, and I weren’t even aware that there was insurance available beyond the widely publicized Marketplace plans. We discussed plans with Mark’s insurance agent (who was doing us a favor; her company doesn’t even sell health insurance any longer, but she offers assistance to clients who buy insurance of other kinds) and decided on the lowest-cost plan linked to a Health Savings Account (HSA). Even those came with a hefty price tag – in 2020, we each paid $799 a month; in 2021, it’s $845 – and it’s a plan coupled with high deductibles. When I say high deductibles, I’m talking about $7,200 per person for one recent year; this year it’s $5,400 per person. Our friend Bert Gilbert, a self-employed general contractor, calls this “don’t-lose-your-house insurance,” the idea being that you pay as little as possible in premiums, considering how expensive even the “affordable” coverage is, and when you need it, the coverage for big ticket items will be there.

Insurance is all about sharing risks, and my one-person design-build furniture business has relatively low gross revenues and profits. Like thousands of other furniture makers, I regard the satisfaction I get from work as part of my “profit,” so every year I’ve signed up for the lowest-cost HSA-linked coverage and hoped I’d never need to use it.

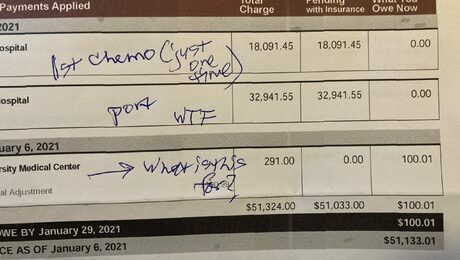

Then came my diagnosis of pancreatic cancer in November 2020. Cancer is one of those big-ticket items. I bided my time, waiting for bills to start coming in and realizing that neither Mark nor I fully understood our health insurance coverage. So one night, when the mail delivered a “billing statement” for $51,000 — $33,000 for my chemo port placement procedure and another $18,000 for just *one* chemo infusion – my stress level went through the roof. I knew the sums were the hospital’s raw charges – they didn’t reflect discounts negotiated by the insurance company, or any actual coverage our insurance company might pay. But even so, I knew we’d be on the hook for our deductibles, as well as the mysterious other charges that together make up our “maximum out-of-pocket expenses.”

This thing could destroy us financially. I seriously considered stopping my treatment right away, until I could get some idea of what it was going to cost. I had inquired about estimated charges before I even agreed to treatment. One oncologist told me, “No one will give you an estimate of charges.” *Friends said “do what you have to, even if you end up paying the hospital $10 a month for the rest of your life” (to which I wanted to respond with another question: If I die, does my husband then lose our house in order to pay the outstanding balance of charges? That’s not a future I want for him, and my life insurance coverage is minimal).

My cousin Gail Hiller-Lee has spent her career in the insurance industry, but I had no idea in which capacity. I contacted her and asked if we could talk. She looked at our policy and gave me the lowdown. Even at the rates we pay, we appear to be responsible for the entire “family” deductible (i.e., even though I’m the one being treated, we have to satisfy the deductibles for both of us) and maximum out-of-pocket charges, the sum of which comes to around $25,000. Gail points out that in a regular/non-HSA-compatible, fully-funded health plan plan through the Marketplace or directly through an insurance carrier, there may be two or three deductibles that each member satisfies individually. But with a high-deductible policy, deductibles are either single (for a one-person plan), or, if the plan covers more than one person, they become a full family deductible, as with ours. (More on this below.)

In our case, this $25,000 in out-of-pocket expenses will be additional to our regular business and living expenses. These charges also come in a year when neither of us will be able to do more than a fraction of our regular paid work — thanks to the pandemic, Mark is the only person I can safely be around in my immune-system-compromised state. Friends have offered to drive me to chemo, etc., but getting into a car with anyone else, no matter how safe they’ve been, is just a bad idea. Ever since March 2020, Mark has been doing fewer jobs than usual, and those have been of less-extensive scope, because he has made a point of not working around other people — for everyone’s sake. Now we’re taking that caution to even greater lengths.

And we thought we were being responsible by maintaining health insurance coverage!

Here is some extensive information and advice from Gail, along with several important definitions of terms.

First, find a broker

“There is a difference between an insurance broker and an insurance agent,” says Gail. “A broker is usually an independent adviser/salesperson who should have no allegiance to any one carrier, offering you [a choice among] everything available. An agent is an employee of a single insurance carrier and primarily sells their employer’s policies but may have the ability to sell other products, as well.”

Everyone who has a car should have a property and casualty broker, ideally someone local whom you can meet face to face, not one of those online insurance companies. When push comes to shove and you have to make a claim, having someone who knows and cares about you can make a big difference. (I know this from experience.) Does your property or business broker have someone in the office who handles health insurance? If not, see whether your life insurance agent can recommend a good health insurance broker.

You may also check with your doctor to see whether they have a broker. If not, their practice may belong to a group that does. Ask for names.

Finally, there are two associations that may be able to help you find a broker: Health Agents For America and the National Association of Health Underwriters. The latter has agents in every state. “Although HAFA has the most dedicated insurance advisers out there,” Gail adds, “they may not have someone in your area.”

Important details to be aware of

Is your network local, regional, or national? If you become ill, your family is in another state, and you have to move in with them so they can care for you, it’s crucial to find out whether there’s a medical care provider there in your network. In “narrow network” plans (such as ours), there’s a local or regional network. National networks are at a premium and may or may not be available. When you’re sick and in an already-challenging situation, finding yourself seeking out-of-network care can be financially and emotionally devastating.

Determine whether your local hospital, urgent care center, and doctor are in a network before you sign up for coverage. You may get an affordable plan, only to discover that no hospital nearby is in the network – not helpful if you have a serious accident at work. While this scenario may sound unlikely, Gail has seen it happen.

Knowing your network is critical, because only charges from in-network medical providers will be covered. If you seek care at an out-of-network facility, you may find that there is no out-of-pocket limit, which can prove disastrous. And if you do have to go to the hospital, don’t just show them your health coverage card; make a point of asking “Do you participate in my insurance?” Then Gail says, “make sure that they participate in the particular network of the insurance plan you purchased.” Otherwise, you could be left with hundreds of thousands of dollars in bills that are not covered. Gail offers an example: “You call your doctor and ask if they are in Blue Cross. They say ‘Yes.’ Blue Cross has MANY networks; your doctor may take one out of the six [or however many] available. They may also say they take your insurance, but if you have both in-and out-of-network coverage, they may take your OUT-of-network portion, leaving you paying thousands before coverage even begins to pay for anything.”

Again, Gail urges, don’t just check a doctor’s or hospital’s website to see whether they participate in your network. Call the doctor or hospital and ask to make sure they are current in their network participation. Be proactive – triple-check! In some cases, even if the umbrella organization, such as a hospital, does, there may be particular departments that don’t. Even if you have a doctor who says they do participate, it’s still worth a call to confirm.

Maximum out-of-pocket expense and related terms

Among the most important innovations of the ACA are (1) an annual cap on out-of-pocket expenses, and (2) lifetime unlimited benefits. Years ago, I happened to notice that one of my policies had a maximum lifetime benefit of $1,000,000. That may sound like a lot, but if you find yourself with serious heart problems, cancer, or any number of other treatment-intensive health conditions, you can burn through a million dollars in coverage all too fast.

Calendar year or policy year

Check the wording of your policy. Any annual cap on out-of-pocket expenses will relate to one of these, but it’s important to know which one applies. A calendar year runs from January 1 to December 31; a policy year can run from the month you buy the coverage to the end of the twelfth month after. Knowing where you stand will help with financial planning.

The maximum out-of-pocket expense and the time to which it relates will have a bearing on what you have to pay. These expenses include:

It’s important to check with your insurance company to make sure that the services you seek are “approved” and covered. If you have to pay 100% for a service, it may count toward your deductible, but not all services will. Uncovered services, which can amount to hundreds of thousands of dollars, will not count toward a deductible.

You may also have co-pays after meeting your deductible. No matter what your co-pay is, it goes toward your maximum out-of-pocket expense for the policy or calendar year, depending on how your policy is worded. Note that high-deductible health plans (HDHPs) always have the deductible apply before any co-pays, but in a non-HDHP you may only have co-pays for general care and never have your deductible apply. Example: You have only office visits and drugs all year and you only have co-pays. The deductible might only apply toward advanced imaging and hospitalization, which you may not need.

After you hit the maximum out-of-pocket expense, the insurance company pays 100% of all additional “approved charges” for that year, “approved charges” being those OK’d by the insurance company prior to the provision of those services.

Another important note on “policy term:” Illness and injury are no respecters of the calendar. It’s common for medical treatment to stretch from one calendar year into another. When it comes to which claims will be considered for coverage in a given year, what matters is the date of service, not when you receive the bill for that service. The charges will go toward the deductible and maximum out-of-pocket expenses for that year.

And now for some general caveats:

Explanation of benefits

Never pay a bill from anyone until you get the Explanation of Benefits (EOB) from your insurance company. If you don’t receive these in the mail, look for them at your insurance company’s website. (I found about 30 pages of these forms fully completed by the insurance company when I looked up my account online a week ago.) If a hospital or doctor sends you a bill that says you have to pay $X because your insurance company has denied the charge or hasn’t paid it, check with the insurance company. Sometimes this just means the medical service provider hasn’t yet submitted the bill to the insurance company for payment. There have been scams from hospitals and other providers of medical care in which they were paid by patients and billed the insurance company, receiving payment twice.

Pre-authorization

Many services require pre-authorization. Before you or your doctor schedules a service, make sure that it has been authorized. The doctor or hospital should obtain this authorization, but, says Gail, “you can’t count on it. Ask your health service provider to make sure that they have got the authorization, because if a doctor turns out to be out of network and did not get a service authorized, you are ultimately on the hook for those charges.” In-network doctors are responsible for obtaining this authorization, but if you show up for a test and it hasn’t been authorized by the insurance company, you’ve wasted your time – the doctor or hospital won’t complete the service without being paid. (This bit of advice comes from extended-family experience.)

If you have an emergency and go to an urgent care facility that happens to be outside of your network, the charges will probably not be covered.

If you go through an emergency room for emergency care, make sure they note in your file that it’s a true emergency, and it will be covered – anywhere in the country.

If you use GoodRX or a similar service to get the best price on prescriptions, you need to be aware that you can either have the cost of the prescriptions covered by insurance (if it is a covered expense) or GoodRX, at least according to current law. If you go through your insurance company and the charge is a covered expense, the cost will go toward your out-of-pocket maximum. If you buy the medication through GoodRX, it won’t.

Short-term medical policies

Beware of short-term medical policies, which provide an alternative to conventional coverage or coverage in-between plans (say, if you’re changing from one job that comes with health insurance benefits to another). Some states allow these policies. Others don’t. Every one of these policies is different, and they are not subject to the ACA.

High deductible health care plans

This is what Mark and I have. First, if the policy is linked to a Health Savings Account (HSA), you have to make sure you’re actually eligible to open an HSA bank account. Not everyone is. For example, if you’re over 65 or have other insurance, such as Medicare, you won’t qualify for an HSA under IRS rules. Second, the HSA must be open before you receive medical services – until you meet your deductible, nothing besides annual preventive screenings will be covered. The least-expensive premium will likely have a high deductible (yours truly raises her hand), high out-of-pocket maximum expenses *and* the smallest network (though this last one is not necessarily the case) – in other words, the most “affordable” premium may ironically result in your biggest exposure to charges, even when you factor in the cost of your premiums.

For instance, any health plan may only cover generic drugs. In my case, our plan does not cover Neulasta, the drug used widely to stimulate the production of white blood cells in patients undergoing chemotherapy, which can make even minor infections life-threatening. Insurance companies will usually send a notice to the patient and their doctor stating that a medication is not covered. I received one of these notices about Neulasta after my oncologist ordered it. The insurance company sent a document that allowed my doctor to appeal the denial of coverage in cases where the patient’s life is at stake.

In such cases, it’s important to discuss with your doctor whether there are alternative drugs to the one denied. If not, ask your doctor for “supporting documentation” that the drug is in fact medically necessary. A doctor may also appeal a decision or have a “peer-to-peer” with the insurance carrier’s medical doctor on your behalf, to overturn a denial of any kind.

In extreme cases, your insurance broker may ask you to contact your state’s attorney general to initiate a complaint about a denial.

Finally, deductibles come in different varieties. Some are “embedded”; others are “non-embedded.” With an embedded deductible, your out-of-pocket expenses are based on each person in your family, so if only one person had expenses, they have to meet their own deductible – then the plan moves into co-insurance, etc. The family doesn’t have to reach the entire family deductible before services are paid. High-deductible plans often have non-embedded deductibles that can refer to each covered individual or the entire covered family. So in our case, we have to meet the family deductible (because there are two of us in our family, this is twice the nominal deductible, i.e. that oft-cited figure of $5,800, which we thought meant that our deductible, for each of us, would be met at $5,400), in addition to the entire family’s maximum out-of-pocket expenses, before coverage kicks in.

Marketplace versus direct carrier insurance

A few reasons why you might choose to go through the Marketplace, rather than directly to a carrier:

But there are equally compelling reasons for avoiding the Martketplace:

*Note that in many cases you can negotiate with hospitals. Tell them you have a high-deductible plan and ask if they will reduce their charges.

Finally, note that there may be changes to any of this information under the new national administration – even more reason to find yourself a trustworthy, knowledgeable broker before you buy healthcare coverage. Also, as reader Andrew Pellar pointed out, some medical costs may be deductible. Be sure to consult your tax professional.

I am deeply grateful to Gail Hiller-Lee of Bernard A. Hiller, Inc. for this crash course in health insurance.

Get woodworking tips, expert advice and special offers in your inbox

This content was originally published here.

Responses